See also 529 plan investment accounts allow education money to grow tax-free

Parley Vernon went to all his classes and took all his tests like any normal undergraduate student. Knowing he would graduate from BYU with a degree in finance, it seemed he would have a successful career path. But Vernon always knew he wanted to return to school for an MBA.

How could he go through the expenses of an MBA when he was just about to finish paying for his undergraduate degree? Expecting to pay double the cost of undergraduate tuition for his MBA, Vernon had to look into his options. Luckily, his finance-savvy mind and interest in all things investing led him to the perfect option — a 529 investment plan. The plans were created to provide a tax-free way to save for college education expenses.

“Just the name itself seems to not really represent what it is. When you think about it, there’s 403Bs and 401Ks and 529s — the numbers confuse families,” said Private College 529 Plan President and CEO Robert Cole.

But 529 plans don’t need to be confusing. The 529 investment plan gets its name from Section 529 of the Internal Revenue Code, the tax code that makes “qualified tuition programs” tax-exempt, according to savingforcollege.com.

The plans come in 2 types: college savings and prepaid tuition. While the two plans have different advantages, they both provide tax-free growth on the money invested if it is used for approved education expenses. Approved education expenses can cover more than tuition; depending on the plan, it may cover housing, meal plans, books and other mandatory expenses, as stated by savingforcollege.com.

Like any investment, the sooner the funds are in the account, the more time they have to grow and the greater the returns. Vernon, now an investment associate at Wasatch Storage Partners, said, “529 plans are more valuable during periods of high return because you get more tax savings, but the beauty of the stock market is you never know what you’re gonna get.”

Vernon said contributing to an account, even for a short time, still benefits education saving. And while Reagan Curtis, a BYU student currently using a 529 plan, agrees that even a small amount of growth is helpful, she said it’s more beneficial if the plan has more time to grow. She said she would recommend the plan to young parents more than she would to current students looking at graduate studies.

According to Vernon, these college savings and investment plans are set up so you can’t really overgrow them. There are account maximums, which vary by plan, but even if participants don’t meet the maximums, extra money in the account doesn’t have to be a problem.

Typically, the account owner can change the beneficiary once per year, according to Reyna Gobel, a contributor at U.S. News. This means the funds can be transferred to the next child in line for education or used to further the account owner’s education if they choose to do more school. Essentially, the plan is set up so the funds are never lost.

If more money remains in the account than the beneficiary needs for their education, the funds can be used on a new beneficiary. Savingforcollege.com says leftover funds can often be moved into a whole new 529 plan account. If a parent has a 529 plan for each of their children, and the oldest doesn’t use all of their funds, the money can be moved to the account of any of the other children.

Vernon said it’s hard to overestimate how much you money one should invest in the account to have money left over after school expenses.

“I think it’d be a little bit hard to really overestimate,” Vernon said. “If you put in for just tuition, I think you’ll be just fine not putting too much in.”

The investment plans positively affect students in more ways than the safety of not losing funds. Curtis said even her account that she started a few years ago has already grown to cover almost a full semester of tuition at BYU.

To cover more than just one semester of tuition, Vernon began saving just after his undergrad, knowing he was set on an MBA. As soon as he had a full-time job, he opened a 529 plan and started making payments toward his further education. When the time came, he covered most of his costs through the 529 plan account he had been paying into for three and a half years. But Vernon said he still paid some out of pocket.

“I was expecting to. I guess I didn’t want to have too much left in there cause I’m not planning on going back to get a doctorate any time soon,” he said. “I’d rather err on the side of having too little than too much, so I still paid some out of my other accounts, but I was totally fine with that.”

Curtis said knowing she had the money allowed her to save for other things that enriched her educational experience. She chose to use her personal savings on things like a study abroad and an internship. Curtis is currently interning at the Youth Refugee Coalition in Salt Lake City and went on a study abroad to Europe in Spring 2016.

Aside from peace of mind about paying for tuition and increasing student savings, a study done by Jaehyun Nam and David Ansong with Economics of Education Review looked into the relationship of parents saving for children’s future education and the likelihood of those children attaining a 2 or 4-year college degree.

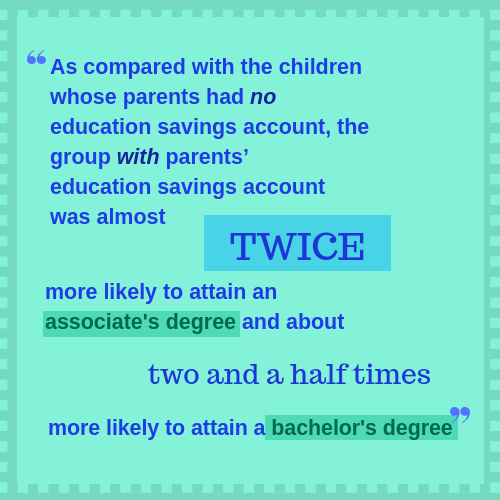

The study showed that “compared with the children whose parents had no education savings account, the group with parents’ education savings account was almost twice more likely to attain an associate’s degree and about two and a half times more likely to attain a bachelor’s degree.”

The study found that when students have a plan or start focusing on higher education sooner, it helps carve out the path for them to get to that higher education. But it also outlined additional benefits.

“The presence of an education savings account may have convinced them that money in the account would remove educational expenses as a major barrier to their college education, and this might have enabled these children to think of a college degree as within their reach as well as to think of themselves as a college-bound student,” the study reads. “As suggested by the possible selves theory, such thoughts about what is possible are powerful motivation for students to work hard to achieve the academic success required to realize their dreams of being college graduates.”

Curtis agreed with the study, saying it helped her take her education more seriously and think about what she needed to do on her own to prepare for college, alongside the 529 plan.

Considering this, why doesn’t everyone use a 529 plan to pay for their education? Curtis said she believes many people aren’t aware of the 529 plan because they are scared of investing and aren’t aware of most of the investment options available to them.

“I think people get a little overwhelmed by the idea of investing because it feels risky,” Curtis said. “But in reality, a 529 is not risky.”

In harmony with Curtis’ beliefs, Vernon said his 529 plan made him feel like he had complete control of the account. He said he chose to be riskier with his investment based on his personality and beliefs, but that everyone can decide exactly how risky or safe they want to be with their own 529 plan.

Both Curtis and Vernon expressed satisfaction with their 529 plan experience and would explain these plans to their future children.

“If you know you want higher education … then you need to take advantage of every resource that will allow you that opportunity,” Curtis said. “A lot of education revolves around money, so anything that you can do to put yourself in a better position to get more education or higher quality education is a huge asset.”

{kind=link}